About Life Insurance With LTC

– Planning for the future.

What are the benefits of a Life/LTC policy?

If you never use your Life/LTC policy for long term care, or use part of it, then whatever is left becomes a tax-free death benefit for your estate.

The Life/LTC policy will pay for home care, assisted living, memory care and skilled nursing (nursing home). Insurance can help you stay at home longer becuase you will have more money for care.

Policies that offer a joint plan are shared benefits and either or both spouses can use the benefits.

Watch Life/LTC video: "There for Generations"

Companies will differ on how they configure the long term care benefits and death benefit. One company might have better LTC benefits and another might have a better death benefit.

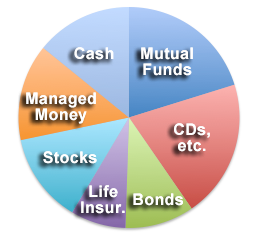

If long term care services are needed, which assets would you use first?

Typically you would use cash reserves for long term care

expenses because cash are usually the lowest yielding and most

accessible. Instead of earmarking an entire account (or more) for long

term care expenses you can reallocate a portion of the cash reserves to

purchase a life insurance policy with long term care benefits.

What are the health requirements?

Just like other insurances, you need to buy this insurance before you need it.

If the policy you are considering has a long term care rider then you

will be underwritten for both life insurance and long term care.

If you have any health conditions that you think might disqualify you then disclose this to the agent you work with. The agent will then be able to guide you to the product that provides the best coverage based on your health.

If you are considering any change in your medications you may have to wait until after you have been on the medication for a while before applying. If you have surgery planned then you should wait until you have recovered before you apply for insurance. Consult with your agent regarding any waiting periods related to health.

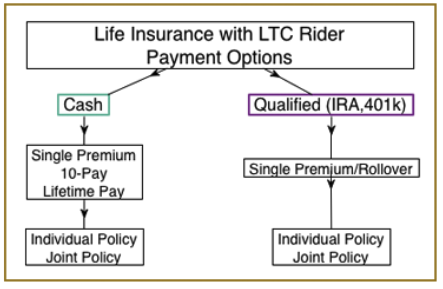

You can pay for your policy with cash or from a qualified account. |

You can re-position existing money such as CDs, Money Market, Savings, or you can 1035 exchange an existing universal/whole life insurance policy. See the Pension Protection Act for more information.

Q: Can I use my IRA money or one of my old 401k's to fund the plan?

A: If you are over 59 1/2 and if available in your

state, you can do a 1035 exchange or "trustee to trustee transfer" to

re-position the money to fund the policy from a 401k/IRA account, you can

fund the policy from multiple "qualified" accounts but they have to be

the same owner. Also, spouses can share benefits even if spouse is under

59 1/2 years old. (shared/joint benefits not available in all states)

Q: I am facing a RMD next year when I turn 70 1/2, will I be able to use the RMD to pay for my policy?

A: Your RMD (Required Minimum Distribution) will

automatically be taken out of your qualified account to pay for the

premium. Depending on how much your RMD will be would determine if you

needed an additional distribution. LIMRA RMD Calculator

What if I already have life insurance?

If you already have a cash-value life policy, you can move the accumulated cash in the old policy to your new policy with LTC benefits without paying any capital gains tax.* This does not apply to "term" life insurance, "term" life has no cash value.